Many individuals, such as yourself, come to us that have been working as mid to high level executives in the corporate sector for the last 15, 20 years (many since college) but have grown tired of it. You want to explore options that allow you to pursue your dreams and other interests. A lot of those revolve around establishing your own business, accompanied by feelings of excitement and fear. “Many people pursuing entrepreneurship have to balance their dreams with their needs,” says Candice Caruso, President of Pango Financial, a small business funding provider. It is exciting to think about being your own boss after many years of having to answer to someone else. But, with that excitement comes fear because you are the primary breadwinner in your family. Between your salary and your options and hefty bonuses, the family relies on you for their lifestyle. It is difficult for you to leave the corporate environment and to give up that level of income, but at your core you are not fulfilled. You are not happy.

There’s no real work/life balance in working 60, 70, 80 hours, traveling, lacking quality time with your family, but you are doing it. Your families have come to expect it and their lifestyles demand it. You don’t really see any way out. What we try to offer you is a safe place to pursue other options by creating a parallel program. Many of our clients have money tied up into old 401K plans, IRA Rollovers from former employers, and other long-term savings vehicles instead of significant cash savings. If they have cash savings, it’s usually earmarked for other things.

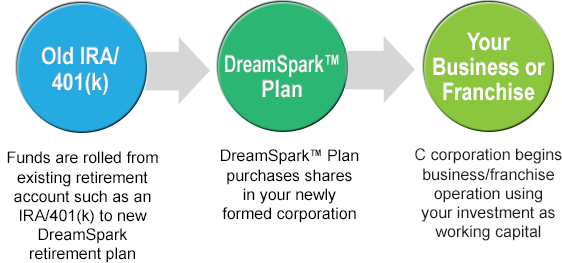

Starting a new business of course costs money. It requires seed capital, especially if buying a franchise, which may be anywhere from $100,000 to upwards of $300,000 to get started. But a little known solution called a ROBS Plan, rollover for business startups, can address the startup problem. “Many people assume their retirement assets are untouchable, but in reality, they can be used today to invest in a business,” says Candice. In this type of plan, tax-deferred assets from a 401k or IRA is used to fund the business. The money is transferred directly into an Employer sponsored retirement plan, the ROBS plan. The ROBS plan uses that capital to purchase shares in the new company. An initial valuation of the business occurs based on the amount of the rollover and that determines the value of the shares that the newly created retirement plan holds. The cash value of those shares is then transferred to an account in the business’ name at local bank and it becomes the business’ operating account. That account can pay the franchise fee (if applicable), pay rent, guaranteed income for the owner, staff salaries, etc.

Below is a graphical illustration of how it works from our friends at Pango Financial.

One of the strengths of this arrangement is that it remains a tax-deferred vehicle. Instead of owning mutual funds, exchange traded funds, or other publicly traded securities in your IRA or 401K, you own shares of your own company. The obvious risk is that if the company fails, then you lose that capital, but you are betting on yourself. Candice says their clients “recognize that risk accompanies any kind of investing, but ultimately entrepreneurs prefer to bet on themselves.”

Below is a snapshot of the pros and cons of this plan:

PROs

1) Immediate access to capital. In my experience, access to capital through this option can take a couple of weeks.

2) Avoidance of high interest rates. A loan with the SBA will still cost you 6% – 8.5%. A private loan would be more.

3) Maintain tax deferral on the money and avoid costly penalties.

CONs

1) Removal of retirement savings from the market to invest in yourself. This can cost you market returns and if the business is not successful, permanent impairment of capital.

2) The company needs to be created as a C corporation for this to be legal. This can remove some flexibility as a business owner.

A ROBS plan isn’t right for everyone but it does provide a unique option that you can pursue if you wanted to start your own business and do not have the necessary capital. Because of its complexity and specifically worded plan document, it is essential that you engage a professional third party administrator who is well-versed in these arrangements.