The Solo Practitioner Plan for Retirement

You’ve set up your own professional practice because you have a vision for your business. You take the risk; you accrue the spoils. But it doesn’t mean you can’t participate in some of the retirement planning benefits of a larger firm, like a 401(k). There’s a specific type of 401(k) that is just for solo practitioners – literally. You can only contribute if you don’t have any other full-time employees. The IRS calls it a “one-participant 401(k),” but it’s commonly known as a solo 401(k).

Because you are both the employer and the employee, the solo 401(k) allows both of your working selves to contribute. And that one-participant thing? In a typical IRS wrinkle, your spouse can actually work in the business — and contribute. There are of course some basic set-up requirements and ongoing responsibilities, but they are not as onerous as for a plan with multiple participants. The benefits may be worth it for your practice and your retirement

Breaking Down the Basics: Contribution Benefits First

The benefits are pretty significant. Even if you are close to retirement, the contribution limits are high enough that you’ll be able to build savings quickly – especially with the employer contribution.

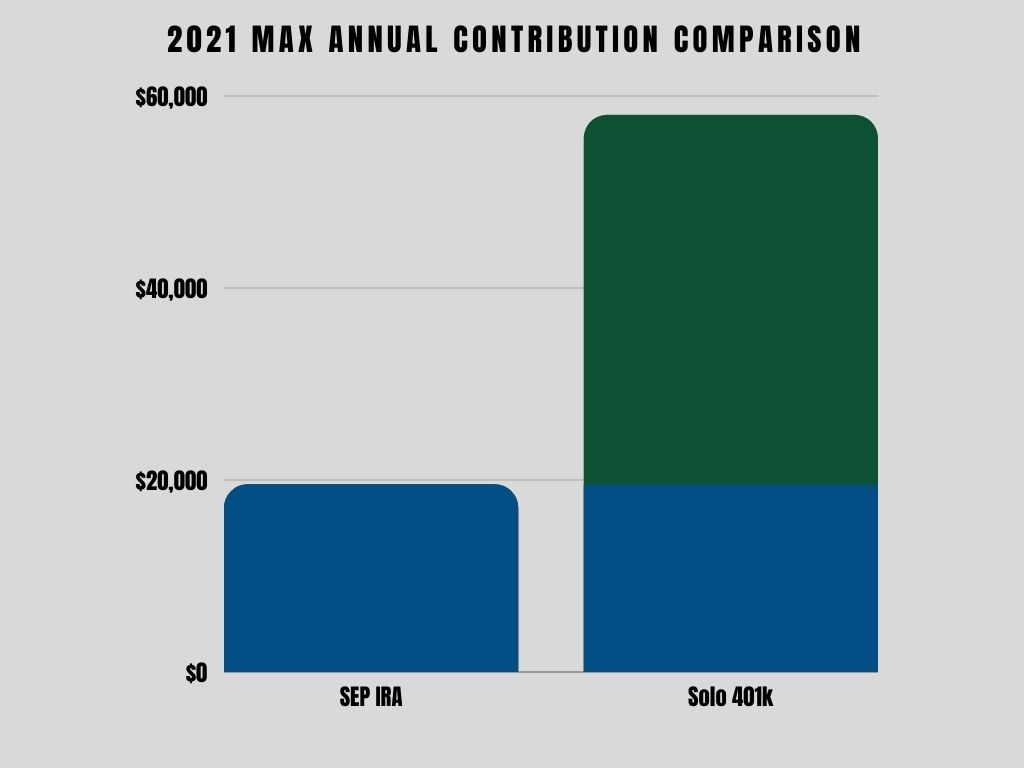

Your employee self can contribute up to $19,500 in 2021, and if you’re over 50 you contribute an additional $6,500 for a total of $26,000.

Since you’re the boss of you, you can also make an additional profit-sharing contribution of up to 25% of compensation or net self-employment income (the IRS defines this as your net profit less than half your self-employment tax and your employee-hat plan contributions). There is of course a limit on the amount of compensation – it’s $290,000 in 2021. But to spare you from some math, the total limit as both employee and employer allowed is $58,000, or $64,500 if you are over 50 in 2021.

And if your spouse earns income from the practice, they can make the same contributions. Double the investment plan, double the tax impact.

This clearly makes it more advantageous than a Sep-IRA. A Sep-IRA only allows for the employer contribution, so you miss out on $20,000 of additional tax-deferred savings. Even if you are unable to contribute that much to the plan, there are additional benefits, which I explain later, that make it more beneficial than a Sep-IRA. The Sep-IRA has been the traditional account for one-man shops.

About Those Taxes

The employer contribution is tax-deductible to your practice, with any earnings growing tax-deferred until withdrawn. The employee portion can reduce personal taxes, but you get to decide when. You can choose to make them to a traditional 401(k) and take the tax savings now, or you can make some or all of your employee contribution to a Roth 401(k), where you pay taxes up front, but your distributions aren’t taxed. Whatever you decide, keep in mind, you can always convert to a Roth later if you choose the traditional method. In both cases, you’ll be following the same rules that would apply to a regular 401(k). You’ll be penalized for early withdrawals before age 59 ½.

Benefits

Since it is a 401k plan, you have some of the benefits available to you as you would a traditional 401k with a large firm. One of these benefits includes the ability to borrow against the plan. While I wouldn’t recommend this as your first line of attack if you were in need of money, it is comforting to know that it is available to you. You can borrow against the plan and pay yourself back over 5 years. This eliminates the need to have to withdrawal from IRAs and incur penalties and taxes.

The other benefit of the plan is that you have the ability to add a Roth provision to the plan. If you are a high-income earner and you are not eligible for a Roth IRA, you can add a Roth provision to the plan. Your employee contributions can be made to the Roth and you will receive all the great benefits that the Roth has to offer and plus you can contribute much more than the $6,000 to a Roth IRA. Just remember, if you choose to contribute to the Roth, you do lose out on the current year’s tax deduction.

What Are the Set-Up Requirements?

It’s best if you have an Employee Identification Number, but you can use your social security number if that’s how you file taxes. The documentation is fairly straightforward, and the deadline to set it up is the end of the calendar year. You have until your tax filing deadline (including extensions) to contribute but the plan must be established by the end of the calendar year. You’ll want to carefully consider you’re practice income, both last year and in the future before, you determine what type of plan to set up. Since you have control, you’ll have the ability to determine what you want to invest in. It’s a great opportunity to review your entire portfolio and put investment savings to work in a way that makes sense from both a risk and a growth perspective across all your assets.

Wrapping It Up

Even if you haven’t given thought to a traditional retirement plan, the benefits of the solo 401(k), and the ability to get one in place this year, are worth a second look. The tax savings and the ability to select your own slate of investments to build your retirement savings make a compelling argument to add one as a small business owner.